|

1

|

- 2013 Essential Charity Law Update

|

|

2

|

- Federal Budget 2013

- Other Recent Federal Initiatives

- Highlights of Recent CRA Publications

- Corporate Law Update

- Selected Case Law

- For more information on these topics, please see an article by the

author titled “Essential Charity Law Update” for the Law Society of

Upper Canada at http://www.carters.ca/pub/article/charity/2013/tsc1112.pdf

|

|

3

|

- On March 21, 2013 the federal government announced the 2013 Federal

Budget (“Budget 2013”)

- The Budget included a so-called “First-Time Donor’s Super Credit”

(“FDSC”) to encourage new donors

- However, the Budget included little from the Standing Committee on

Finance (“SCOF”) Report, which was released in February 2013 and was

intended to be taken into consideration for Budget 2013

- Given the present economy, the charitable sector is lucky that there

were any new charitable donation tax incentives at all included in

Budget 2013

|

|

4

|

- Hopefully, some of the other recommendations from the SCOF Report will

make their way into future federal budgets, such as the “Stretch Tax

Credit for Charitable Giving” proposed by Imagine Canada

- A portion of Budget 2013 was implemented on June 26, 2013 through the

enactment of Bill C-60, Economic Action Plan 2013 Act, No. 1

- Portions of Budget 2013 were implemented through Bill C-4, Economic

Action Plan 2013 Act, No. 1, which received Royal Assent on December 12,

2013, while other provisions in Bill C-4 are to come into effect at

later specified dates

|

|

5

|

- Temporary One Time Donation Tax Credit for “First-Time Donors”

- This new tax credit, implemented through Bill C-60, is designed to

encourage donors who have not donated within the last five years to give

to charity and is only available where neither a donor nor his or her

spouse or common-law partner has claimed a charitable donation tax

credit in the five previous tax years

- When applicable, there is to be an additional one time 25% tax credit

for “first-time” donations of up to $1,000 of a gift, provided that the

gift is made in cash

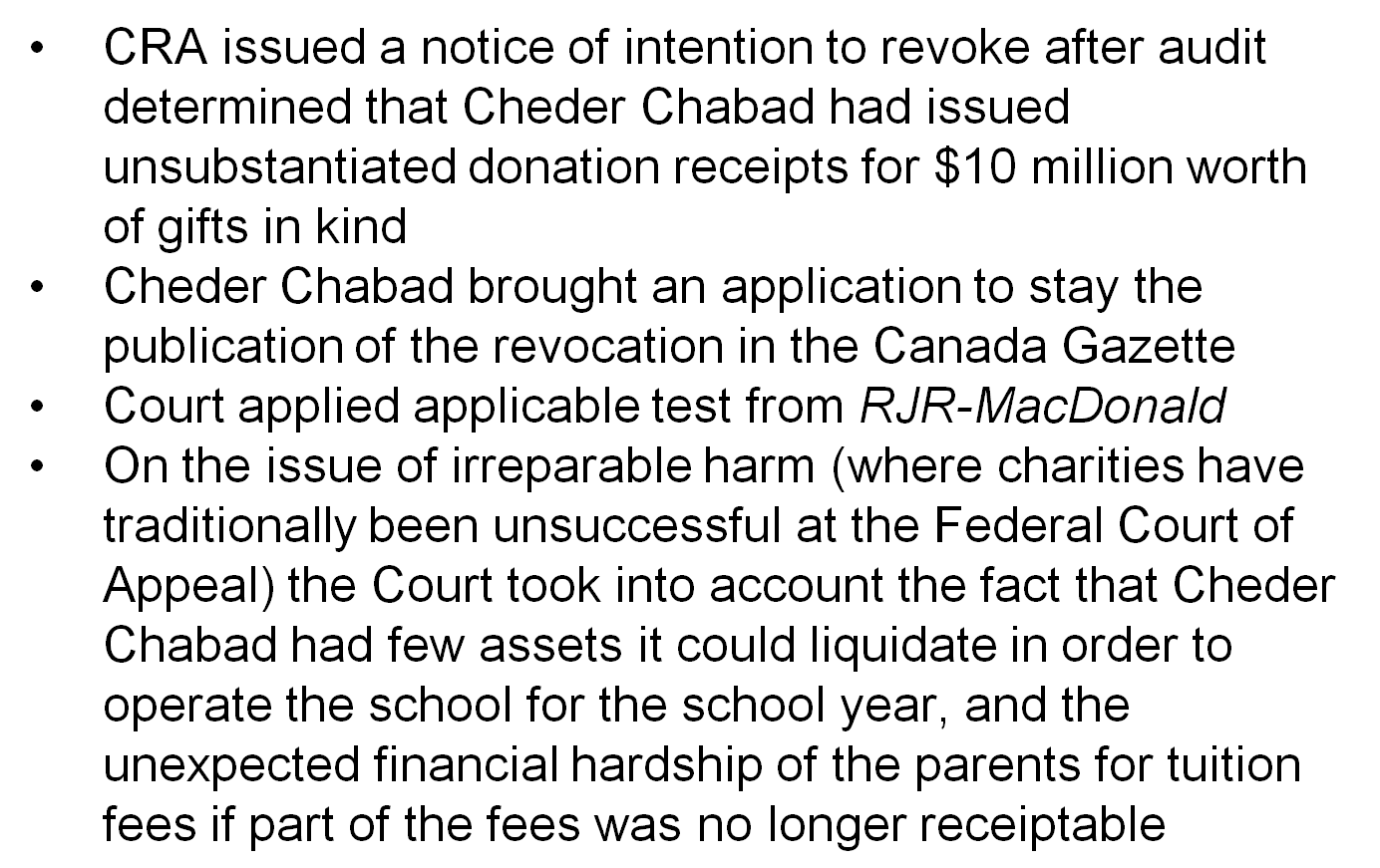

- Therefore, for a gift of $1,000, an additional tax credit of $250 is

available

- However, the FDSC can only be claimed once between 2013 and 2017 tax

years

|

|

6

|

- Early Collection of Amounts Owing from Donation Tax Shelters

- Bill C-60 permits CRA to proceed with collection actions on 50% of the

disputed tax, interest or penalties that result from the disallowance of

a donation claimed with respect to a tax shelter

- CRA will be able to proceed with these actions even before the ultimate

liability of the donor has been determined through the objection and

appeal process

- While donation tax shelter schemes should be discouraged, it is arguably

unfair to permit CRA to collect taxes, fines, and penalties before the

tax payer has exhausted all avenues of appeal

|

|

7

|

- Extension of Reassessment Period for Donors to Registered Tax Shelters

- As part of its effort to balance the budget, the federal government has

taken a hard line on various tax loop-holes, particularly those

involving tax shelters

- This change, set out in Bill C-4, is deemed to have come into force on

March 21, 2013, and extends the normal reassessment period with respect

to participants in a tax shelter or “reportable transactions” where the

information return required to be filed by the tax shelter or reportable

transaction is not filed on time, or at all, by a period of a further 3

years after the date that the information return has been filed (for a

total of 6 years)

|

|

8

|

- New Rules Concerning Collection of GST/HST on Paid Parking Affecting

Charities

- As of January 1, 2014, Budget 2013 (Bill C-4) will amend the Excise Tax

Act to clarify that public sector bodies, i.e., municipalities,

universities, public colleges, school authorities, hospital authorities,

charities, non-profit organizations or government are not exempt from

collecting and remitting HST/GST on supplies of paid parking

- Repeated Focus on Transparency and Accountability in the Charitable

Sector

- The federal government will encourage donations and further enhance

public awareness, reduce red tape, and increase transparency and

accountability in the charitable sector, by working with organizations

in the sector, including Imagine Canada

|

|

9

|

- Federal Government Recommits to Supporting Social Finance

- The federal government will continue to “bring together key players in

the non-profit and private sectors to develop investment-worthy ideas

and tap the potential of the social finance marketplace to promote

economic growth and prosperity”

- Amalgamation of the Department of Foreign Affairs and International

Trade with CIDA

- The Department of Foreign Affairs and International Trade and the

Canadian International Development Agency were amalgamated into the new

Department of Foreign Affairs, Trade, and Development (DFATD)

|

|

10

|

|

|

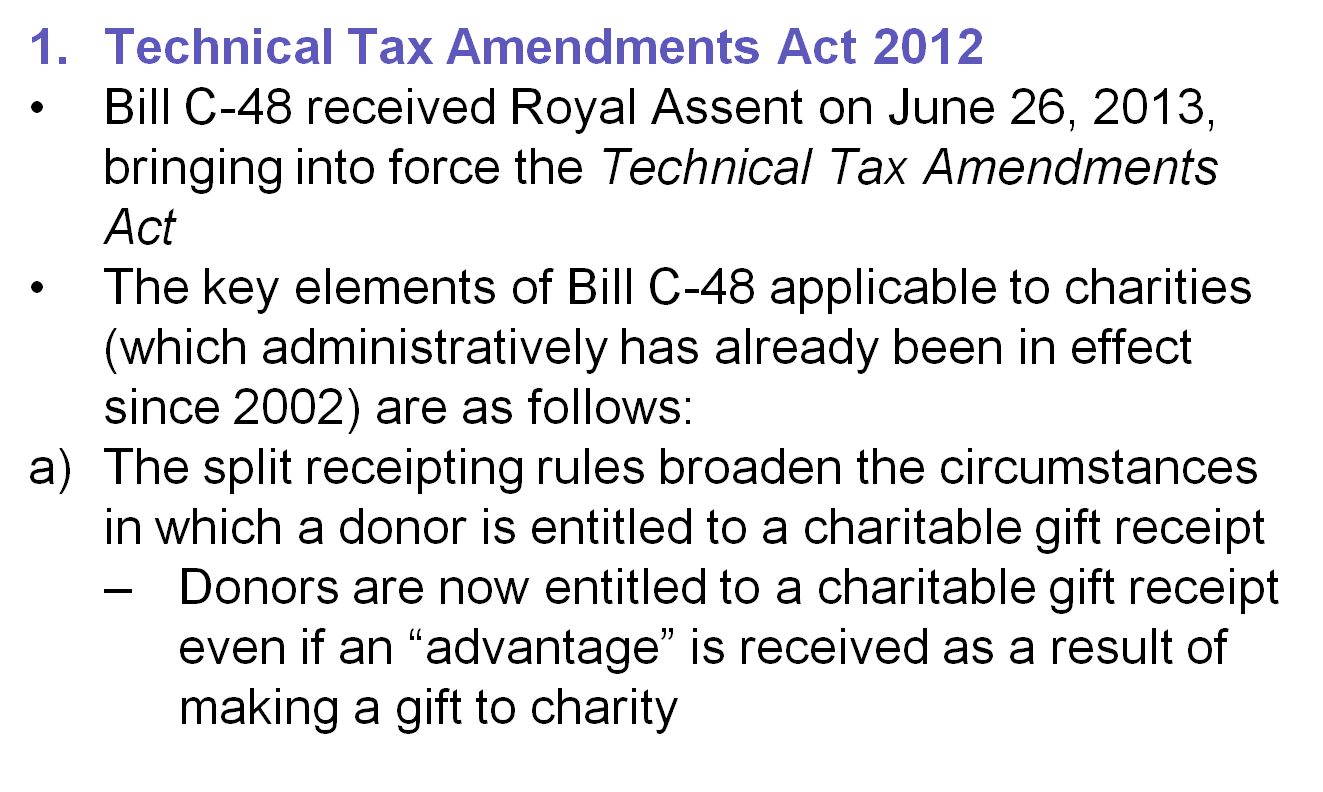

11

|

- The amount of the gift is the “eligible amount”, i.e., the fair market

value of the property donated minus the value of the “advantage”

- Definitions of “charitable organization” and “public foundation” in s.

149.1(1) were amended

- Large capital contributions from a single person or group of persons

not dealing at arm’s length with one another will not preclude an

entity from qualifying as a “charitable organization” or a “public

foundation”, provided that such person or persons do not control the

charity

|

|

12

|

- There is now an additional basis upon which charitable registration may

be revoked under ss. 149.1(2) to (4)

- Charitable registration can be revoked where a registered charity makes

a “gift” to a person or entity other than a “qualified donee",

- There is an exception where the transfer was in the course of the

charity carrying on charitable activities

- The determination of the fair market value of property that is the

subject of a gift has been changed in the limited circumstances

described in new s. 248(35), (generally where the donor acquired the

property less than three years before making the gift)

|

|

13

|

- Section 6(1)(a)(vi) has been added to provide a new exclusion from the

calculation of a taxpayer’s employment of any benefit under a program

offered by an employer to assist in furthering education provided that:

- The benefit is received or enjoyed by an individual other than the

taxpayer;

- The employee taxpayer deals with the employer at arm’s length; and

- It is reasonable to conclude that the benefit is not a substitute for

salary, wages, or other remuneration of the taxpayer

- The exclusion is retroactive, applying to such benefits received on or

after October 31, 2011

|

|

14

|

|

|

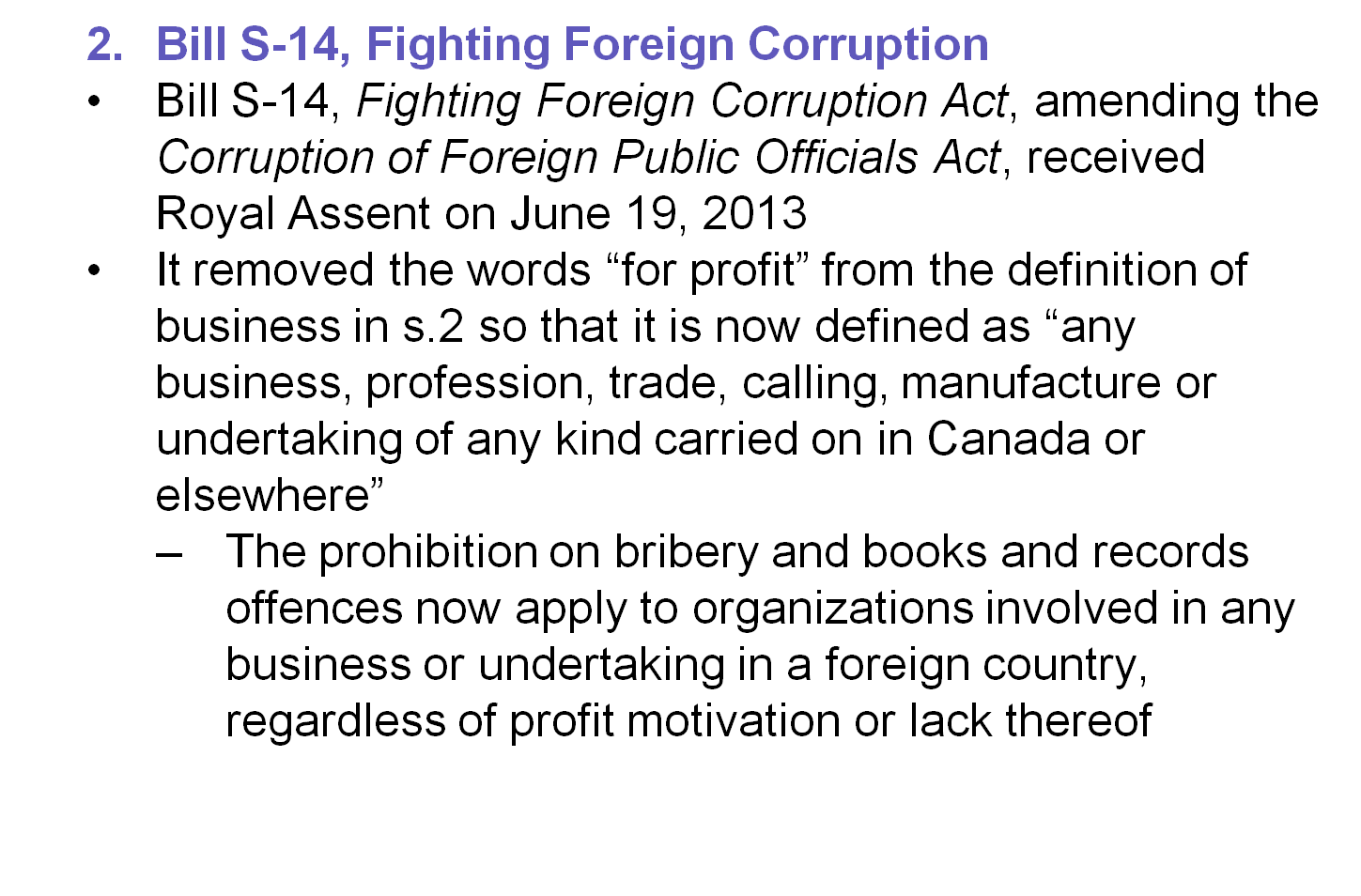

15

|

- This modified definition could impact charities carrying on

activities outside of Canada where their programs in a foreign

jurisdiction include a “related business” activity permitted under the

ITA, or a charitable program that involves an inherently commercial

element, such as microfinance

- A second important amendment will repeal the “facilitation payment”

exemption provision of the Corruption of Foreign Public Officials Act on

a date to be fixed by order of the Governor in Council

- Currently, such facilitation payments are excluded from the prohibition

on bribery

- As a result, in the future, charities could be exposed to possible

criminal liability for activities which, up to now, have been permitted

|

|

16

|

- Bill S-202, An Act to Amend the Payment Card Networks Act (credit card

acceptance fees), received first reading on October 17, 2013

- It proposes to limit credit card

acceptance fees charged by “designated payment card networks” to

merchants who accept payment by credit card, eliminating credit card

acceptance fees being charged to charities

- Currently, only MasterCard and Visa are proposed to be “designated

payment card networks”

- If passed without amendments, Bill S-202 would benefit charities by

allowing donations to be made by credit card without additional credit

card acceptance fees

|

|

17

|

- On December 4, 2013, the Minister of Industry announced that Bill C-28

(the “Anti-Spam Legislation”) will come into effect on July 1, 2014

- The Anti-Spam Legislation will prohibit the sending of commercial

electronic messages unless the sender has consent and the message

contains prescribed information

- Final regulations now provide an exemption for messages sent by or on

behalf of charities that have a primary purpose of raising funds for the

charity

- This is not a full exemption from all commercial electronic messages

from charities

- This exemption only applies to charities (i.e. non-profit organizations

are not exempt)

|

|

18

|

|

|

19

|

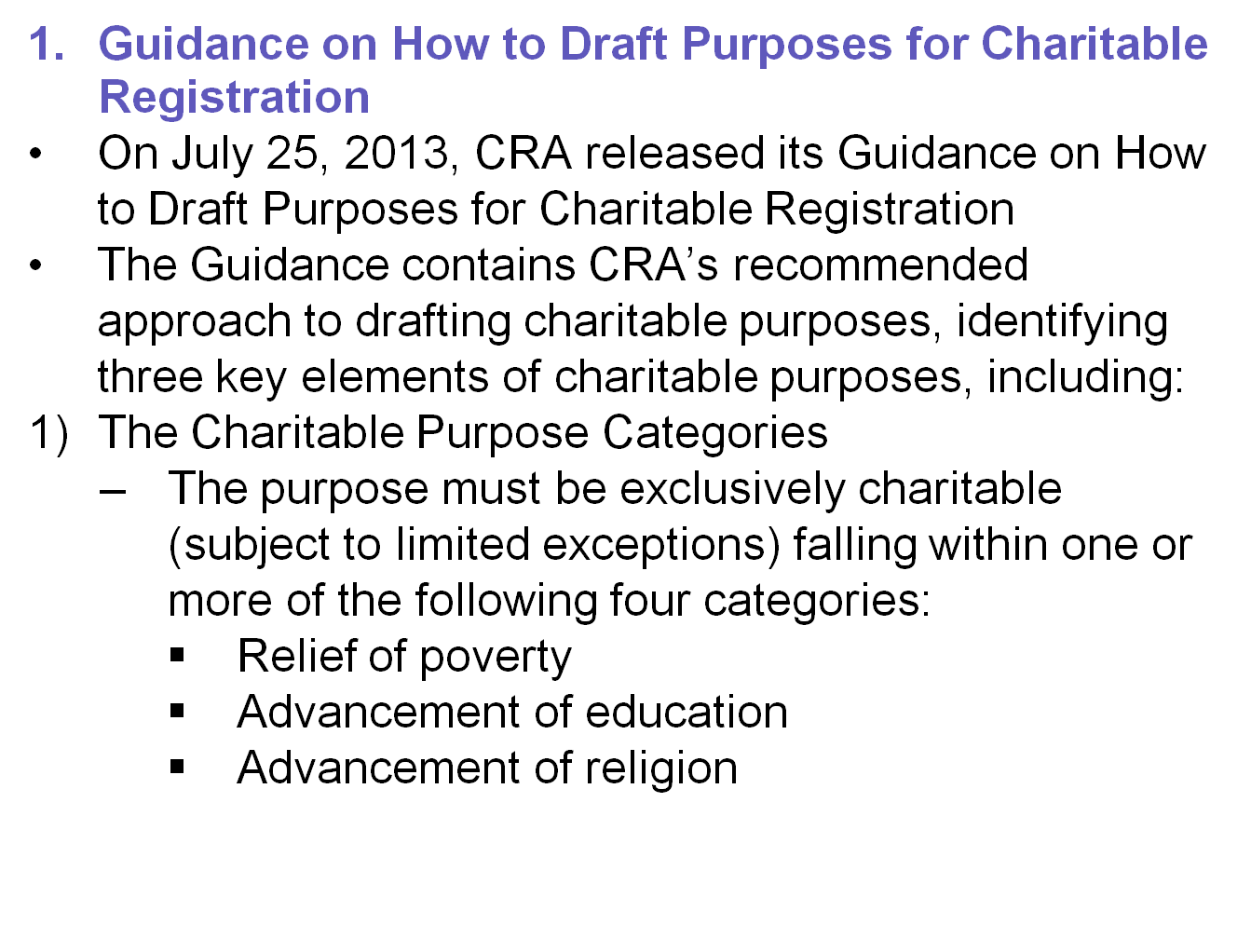

- Other purposes that are beneficial to the community in a way that the

law regards as charitable and provide a benefit to the public or a

sufficient segment of the public

- It can be met by using the wording of the particular category, (e.g.

“advancement of religion”)

- For the fourth category, it is necessary to specify the particular

purpose within that broad category

- The Means of Providing the Charitable Benefit

- The purpose should define the scope of activities conducted to directly

further the purpose and ensure the provision of a charitable benefit

- The Eligible Beneficiary Group

- The charitable benefit should be provided to the public or a sufficient

section of the public

|

|

20

|

- The Guidance provides definitions of the first three categories of

charitable purposes which synthesize a complicated body of case law in

each category

- This appears to be the first time that a CRA Guidance has provided a

definition with respect to the charitable category of advancement of

religion, defining it as:

- “manifesting, promoting, sustaining, or increasing belief in a

religion’s three key attributes, which are: faith in a higher unseen

power such as a God, Supreme Being, or Entity; worship or reverence;

and a particular and comprehensive system of doctrines and observances”

- The Guidance addresses various other factors regarding charitable

purposes:

|

|

21

|

- Charitable purposes should not be too broad or vague so that CRA can

access whether it is exclusively charitable and not open to

interpretation

- Organizations pursuing unstated purposes through activities that are

not charitable are not eligible for charitable registration or

maintaining charitable registration if subject to an audit

- The CRA offers a one-time review of:

- Proposed purposes in draft governing documents of organizations wishing

to attain charitable status

- Proposed amendments to governing documents and a detailed statement of

activities of organizations wishing to amend such documents

|

|

22

|

- On June 24, 2013, CRA Charities Directorate released its Guidance

dealing with organizations that benefit youth

- The Guidance replaces the earlier CPS-015 Registration of Organizations

Directed at Youth

- The Guidance describes how CRA determines whether an organization that

benefits youth is eligible to become a registered charity under the ITA

or presumably can continue as a charity if subject to an audit by CRA

|

|

23

|

- Whereas the former policy defined youth with respect to age, the new

Guidance defines “Youth” as “young people, without restriction to a

specific age range, which will now depend on the nature of the

charitable purposes and activities in question.”

- The Guidance also defines “at-risk youth” as “youth who are in danger of

not making a successful transition to healthy and productive adulthood

as a consequence of a range of possible issues, including, but not

restricted to, learning difficulties, socio-economic environment, social

relationships, and family/school situations.”

- Purposes that benefit youth may fall under any of the four categories of

charity described in the Guidance on How to Draft Purposes for

Charitable Registration

|

|

24

|

- Eligible beneficiaries are those people who may qualify to receive the

benefits from the charitable purpose or from its respective activities

- Purposes may either allow all youth or particular youth to benefit

- The public benefit that is delivered by a charitable purpose needs to be

“a reasonably direct result of the purpose and activities”

- Incidental activities that do not further the purpose will not meet this

public benefit requirement

- An organization must use “substantive evidence of a causal connection”

to show that an activity can provide a public benefit by structuring and

focusing activities to address the identified youth problem

|

|

25

|

- An organization can demonstrate structure and focus through:

- the activity’s form (e.g. structured discussions);

- the communications between qualified individuals and youth; and

- roles and responsibilities of youth in activities (e.g. allowing youth

to participate in supervisory roles)

- The Guidance outlines various examples of charitable purposes and

activities relating specifically to youth:

- Purposes with a “teaching or learning component”

- Social or recreational activities that further a charitable purpose

- Sports activities designed to address youth problems, provided that

there is a causal link between the activity and the charitable benefit

|

|

26

|

- On August 27, 2013, CRA released a new Guidance on the Promotion of

Health and Charitable Registration (CG-021replacing earlier policies)

- The Guidance states that the promotion of health is a charitable purpose

upon which organizations may be eligible for charitable registration

- The Guidance defines the promotion of health as “directly preventing or

relieving physical or mental health conditions by providing health care

services or products to eligible beneficiaries”

- Promotion of health is a charitable purpose under the following two

conditions:

|

|

27

|

- It provides services or products to the public, thereby directly

preventing and/or relieving a physical or mental condition; and

- It must meet relevant requirements for quality and safety

- Additionally, to be eligible for charitable registration, promotion of

health must:

- Be provided only to eligible beneficiaries (the public or a sufficient

section of the public)

- Not provide unacceptable, non-incidental private benefits

- The Guidance divides health related purposes into four categories:

|

|

28

|

- Core health care

- Supportive health care

- Protective health care

- Health care products

- The Guidance discusses special topics related to healthcare which may

further charitable purposes:

- Complementary or alternative health care services

- Physical fitness and wellness

- Providing information as a charitable activity

- Providing medical clinics

- Providing health care services in underserviced areas or areas of

social and economic deprivation

- Charities may charge fees, as long as the fees do not further a profit

purpose

|

|

29

|

- The Guidance states that some health-related activities may further

other charitable purposes as well, such as relieving poverty, advancing

education, and advancing religion in the charitable sense, as described

below:

- There must be “a clear and material connection between the activity and

the religion’s key attributes”

- Eligible beneficiaries are the public at large

- There are two situations in which health‑related activities may

further advancement of religion:

- Providing health care to the public, and by doing so, promoting the

doctrines of a religion

- Providing health care to religious staff, including those retired, in

support of religious contribution or service

|

|

30

|

- On an earlier date (likely in June 2012), Appendix B of CRA Guidance -

CG-002 “Canadian Registered Charities Carrying Activities Outside of

Canada” was amended

- It is now titled “What if a charity wants to transfer capital property

to a non-qualified donee in a foreign country?”

- CRA has now made it much more challenging for a charity operating in a

foreign jurisdiction to transfer ownership of capital property to a

non-qualified donee:

- Transferring such ownership is now only permitted in the following

three circumstances:

- If the jurisdiction in which the charity operates prohibits foreign

ownership of capital property

|

|

31

|

- If the capital property is transferred to relieve poverty by assisting

communities develop into self-sufficient communities

- If the charity has proof that it has unsuccessfully made every

reasonable effort to gift the capital property to a qualified donee

and to sell it at fair market value

- The amendment may also affect the basic elements of a written agreement

between the parties in such situations situation, as set out in Appendix

F of the Guidance

- Appendix F will presumably now need to be read subject to the more

onerous requirements above

|

|

32

|

- CRA released new T3010 forms for charities with fiscal periods ending on

or after January 1, 2013 in response to Budget 2012 amendments (Bill

C-38) requiring that charities give more details about their political

activities

- Bill C-38 amended the definition of “political activity” under s.

149.1(1) of the ITA to include “the making of a gift to a qualified

donee if it can reasonably be considered that a purpose of the gift is

to support the political activities of the qualified donee”

- Bill C-38 also required that charities disclose more information

concerning their political activities

- The new T3010(13) asks if the charity carried on any political

activities during the fiscal year, including “gifts to qualified

donees...intended for political activities.”

|

|

33

|

- A charity that participates in political activities must complete

Schedule 7 and:

- describe its political activities, including gifts made to qualified

donees intended for political activities

- explain how these political activities relate to its charitable purpose

- disclose how it has conducted its political activities

- disclose the political activity that the funds indicated on line 5032

were intended to support and the amount received from each country

outside Canada

- Additionally, CRA has developed a number of pages on its website

explaining key aspects of its Policy Statement CPS-022, Political

Activities to help charities comply with its political activities

requirements

|

|

34

|

- On August 26, 2013, a new CRA webpage was posted to clarify the

important distinction between amalgamations, mergers, and consolidations

- Amalgamations bring memberships, assets, and liabilities of both

charities into one new entity

- The original charities continue as one entity, but are not dissolved

- New entity may choose which of the original charities’ Business Names

(“BN”) to retain

- Mergers involve the winding up of one or more entity’s affairs and the transfer of the wound

up entity’s assets to another registered charity

- Wound up charities voluntarily revoke their registration

|

|

35

|

- BN of remaining charity is not affected

- Consolidations involve dissolution of all original bodies and transfer of

assets to a new entity

- All original bodies are wound up and undergo voluntary revocation of

their registration

- New body is given a new BN

- Charities that amalgamate, merge, or consolidate should inform the

Charities Directorate before doing so

- To initiate a request for an amalgamation, merger, or consolidation,

charities should follow steps outlined online: http://www.cra-arc.gc.ca/chrts-gvng/chrts/prtng/chngs/mlgmtns-mrgrs-cnsldtns-eng.html

|

|

36

|

- Canada Not-for-profit Corporations Act (CNCA)

- Status of CNCA

- Canada Corporations Act (“CCA”) since 1917

- Enacted on June 23, 2009, in force October 17, 2011

- Replaced Part II of CCA

- Existing CCA corporations required to continue under the CNCA within 3

years - i.e., by October 17, 2014

- Failure will lead to dissolution of the corporation

- According to Industry Canada, there are an estimated 17,000 Part II CCA

non-profit corporations.

- As of October 31, 2013, only 2100 or 15% of not-for-profit corporations

incorporated under the CCA had continued under the CNCA

|

|

37

|

- Overview of CNCA Continuance

- New CNCA rules do not automatically apply to CCA corporations (must

apply to continue)

- Charities need to prepare new corporate documents (Articles and By-laws)

- Board and membership approval is required (at least 2/3 for

Articles/check current corporate documents for possible higher approval)

- File required documents with Industry Canada

- Industry Canada will issue a Certificate of Continuance

- Charities must send Certificate, Articles and By-laws to CRA and Ontario

Public Guardian and Trustee

- If not continued by October 17, 2014, Industry Canada will send out

Notices of Intention to dissolve, giving the charity 120 days after the

notice to continue

|

|

38

|

- Basic Framework of the CNCA

- The CNCA is conceptually structured on a business corporate model which

gives enhanced rights of members

- CNCA provides both a general framework and a set of rules for

corporations to operate

- Three types of rules in CNCA

- Mandatory Rules - Cannot be overridden by the articles or by-laws

- Default Rules - By-laws or articles can override

- Alternate Rules - Articles/by-laws can include certain optional rules

provided in the Act

- It is important to be familiar with the rules before drafting CNCA

corporate documents (legal assistance can help)

|

|

39

|

|

|

40

|

|

|

41

|

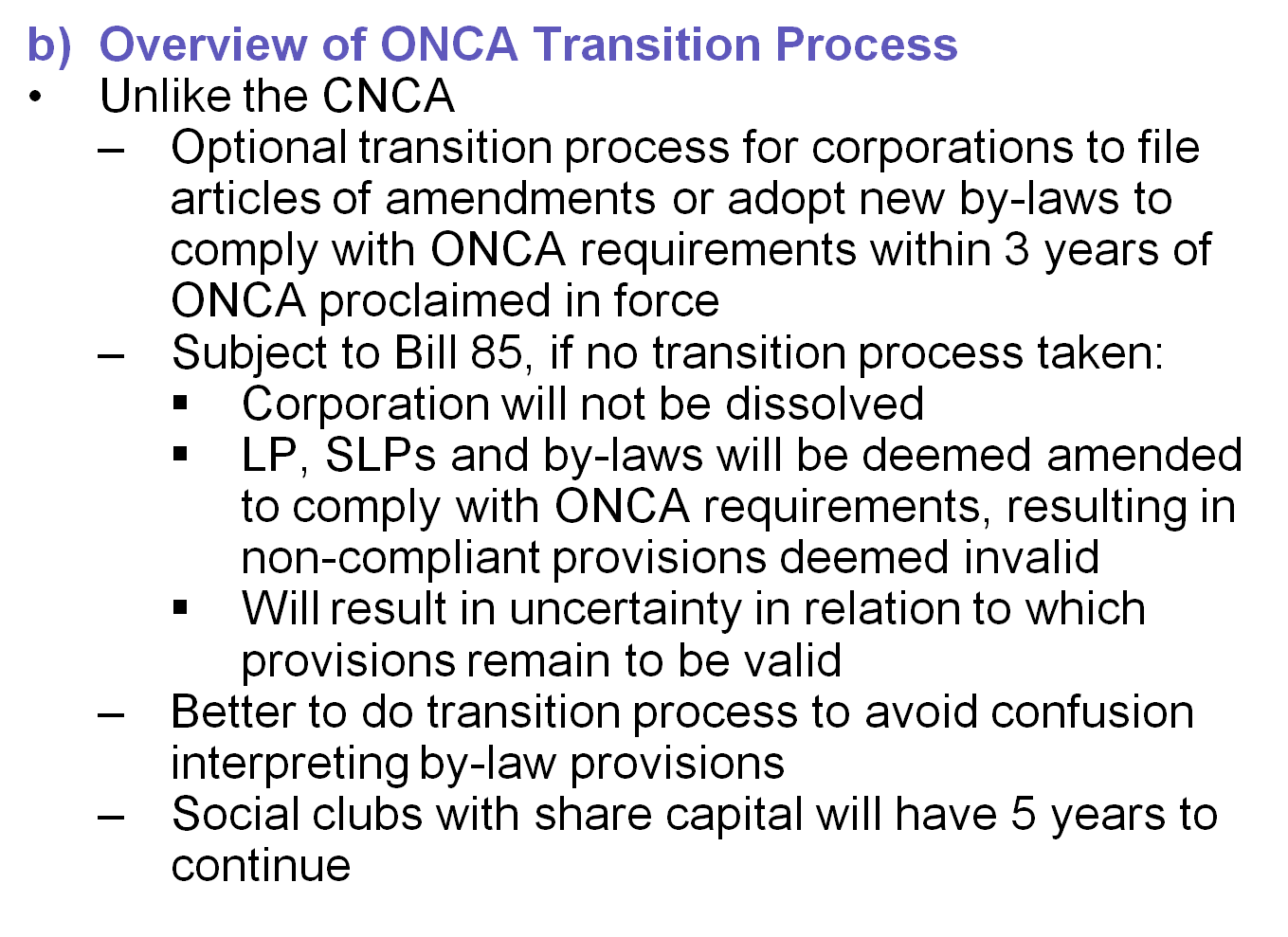

- However, Bill 85, if passed, will provide for the following amendments

to the ONCA:

- The Public Benefit Corporation threshold, currently $10,000, may be

amended by regulation

- All directors must consent in writing, and the corporation must keep

this in the ‘approved form’

- During the 3-year transition period, Part III OCA Corporations must add

to their articles all provisions, by-law provisions, or special

resolutions that the ONCA requires to be contained in their articles

|

|

42

|

- Any amendments to by-laws will require that all by-law amendments be

adopted

- Non-voting classes will have their limited right to vote delayed until

at least three years after the rest of the ONCA comes into effect

- As a general rule, if a special act corporation’s provisions are

inconsistent with the ONCA, the special act prevails

- The ONCA provides that charity law will prevail over the ONCA

|

|

43

|

- B.C.’s Bill 23, Finance Statutes Amendment Act, 2012 took effect on July 29, 2013,

providing for a new type of company called a “community contribution

company” (“CCC”)

- CCCs promote social enterprise, allowing the for-profit sector to tap

into socially focused investment options

- CCCs must primarily benefit the community through:

- restrictions on corporate reorganizations to avoid the circumvention of

payout restrictions;

- an “asset lock” that caps dividends on company shares to ensure that

profits are retained by the company or directed to the community

benefit

- CCCs cannot issue tax receipts, and are not eligible for NPO status

|

|

44

|

- On December 6, 2012, Nova Scotia’s Community Interest Companies Act,

Bill No. 153 received Royal Assent, allowing businesses to seek

designation as a “community interest company” (“CIC”)

- To qualify for the CIC designation, a company must:

- have a “community purpose,” that being a purpose “beneficial to society

at large or a segment of society that is broader than” those related to

the CIC

- have at least three directors who must act in accordance with the

company’s community purpose

- CICs are restricted in their ability to pay dividends and distribute

assets on dissolution, and must either comply with the rules for

non-profit organizations or pay tax as a for-profit corporation

- The Act will come into force upon proclamation

|

|

45

|

- On September 26, 2013, the Ontario Ministry of Economic Development,

Trade and Employment announced “Impact - A Social Enterprise Strategy

for Ontario” to support social enterprises in Ontario

- Social enterprises “use business strategies to maximize [their] social

and environmental impact”

- The Social Enterprise Strategy aims to:

- Connect, co-ordinate and communicate information to, and about, social

enterprise

- Build the social enterprise brand

- Create a vibrant social finance marketplace

- Deliver service, support and solutions

- It is not known when enabling legislation will be introduced

|

|

46

|

|

|

47

|

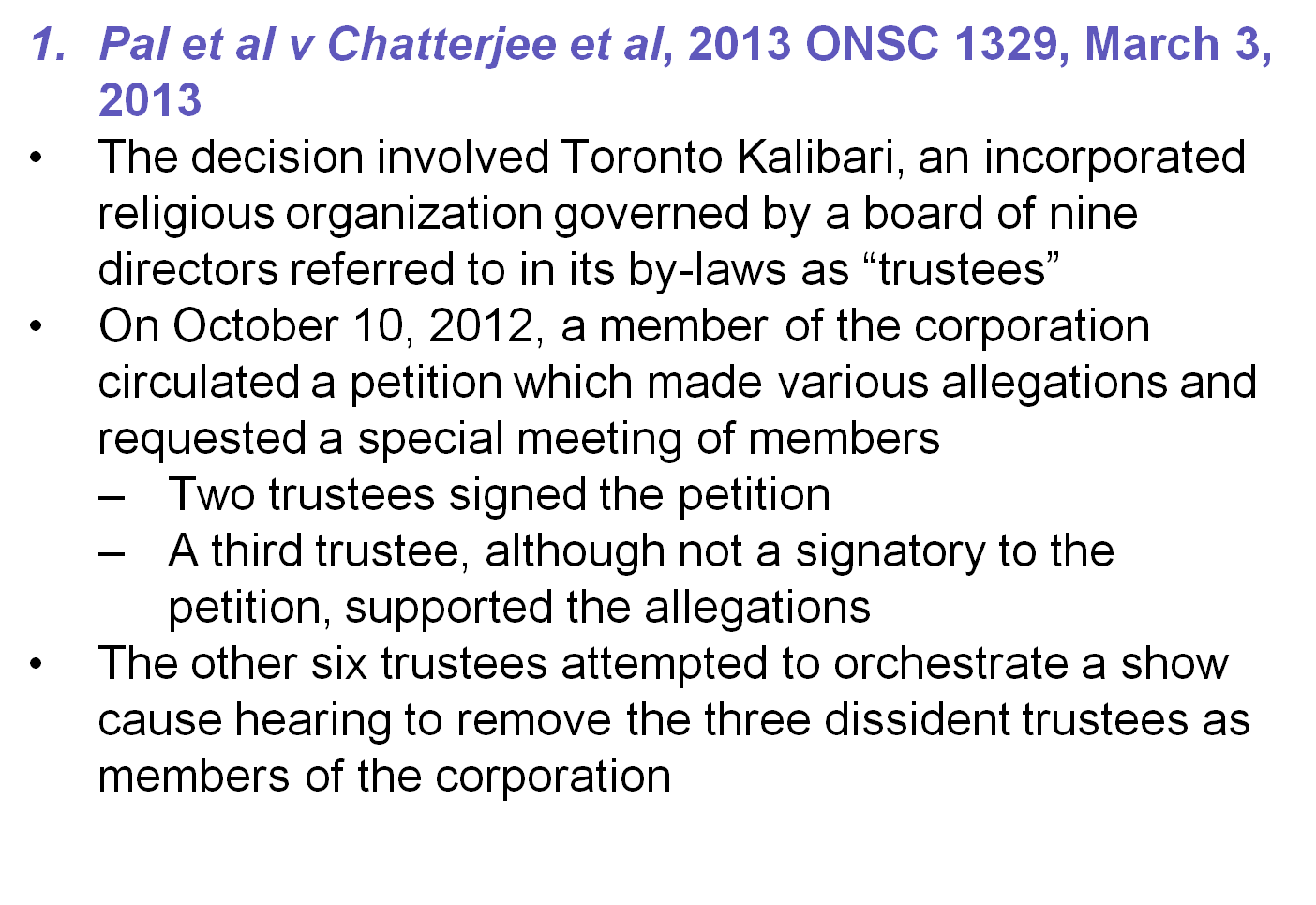

- The court examined the by-laws of the corporation and determined that

there was no method available for the removal of the trustees

- The court found that the termination of the applicants as trustees

warranted intervention and that the show cause hearing was being

initiated for the improper and oblique purpose of their removal

- The decision is a reminder that corporate proceedings to discipline or

terminate a member cannot be commenced for an improper or ulterior

purpose

|

|

48

|

- Diaferia v Elliott was an application for an interlocutory injunction

preventing a membership meeting discussing whether or not a church’s

pastor should be dismissed

- Church membership required members to complete a three-step process

involving an interview, baptism, and confirmation by church membership

vote

- Upon announcement of a meeting of members to discuss the pastor’s

dismissal on March 3, the pastor announced, with support of 5 members, a

meeting to be held on February 24 at which the pastor would ask the

elders to consider membership of those that supported him

|

|

49

|

- The elders, however, decided that only those who had met the

qualification requirements for membership as of February 10, 2013 would

be recommended for admission into membership

- Of 14 applicants, 12 were denied membership

- An injunction was sought and granted to prevent the meeting called for

March 3

- The court sought to ensure that there was a level playing field for both

sides concerning the employment of the pastor

- This case is a reminder that if a procedure for admitting members is in

the organization’s governing documents, it should be followed, and

should be made well known to those who want to become members

|

|

50

|

- Pursuant to a CRA audit in 2008, CRA issued a notice of intention to

revoke Prescient Foundation’s charitable registration based on three key

issues:

- Prescient donated $500,000 to a foreign non-qualified donee

- Prescient was involved in the sale of a farm, where sale proceeds were

routed on a tax-free basis “for the private benefit of certain

taxpayers”

- Prescient had “failed to maintain adequate books and records” by only

providing CRA with several relevant documents and not allowing CRA to

verify information in the Foundation’s financial statements and

registered charity information returns

|

|

51

|

|

|

52

|

- CRA assessed a penalty of $564,747 against Guindon under section 163.2

of the ITA

- Guindon had provided a legal opinion on the “The Global Trust

Charitable Donation Program” charitable donation scheme

- She also issued 134 charitable donation receipts

- S. 163.2 provides for monetary penalties assessable against third

parties who knowingly, or through gross negligence, participate in,

promote, or assist conduct that results in another taxpayer making a

false statement or omission in a tax return

- The Tax Court of Canada (“TCC”) held that the section 163.2 penalties to

be applied were of a criminal nature, as per s. 11 of the Charter

|

|

53

|

- The Tax Court’s decision was overturned on appeal by the FCA on the

basis that:

- Guindon failed to serve a notice of constitutional question when she

sought a finding that a section of the Act was invalid, inoperative or

inapplicable

- The TCC therefore had no jurisdiction to consider whether s. 163.2

created a criminal offence under s. 11 of the Charter

- The FCA also held that proceedings under section 163.2 are in place to

maintain discipline, compliance or order “within a discrete regulatory

and administrative field of endeavour” and are, therefore, not criminal

in nature

- On September 11, 2013, Guindon filed for leave to appeal to the Supreme

Court of Canada

|

|

54

|

- This application was commenced by self-described atheists asking the

Tribunal to consider whether materials explaining atheism should have

the same protection and ability to be available to students as materials

explaining or promoting mainstream religions, such as Christianity or

Islam

- To answer this question, the Tribunal needed to decide whether atheism

should be considered a “creed”, and thus a protected ground under the

Ontario Human Rights Code (“Code”)

- The Tribunal decided that atheism is a “creed” for purposes of

protection under the Code

|

|

55

|

|

|

56

|

|

|

57

|

- On the balance of convenience, the court took into account the impact

that the publication of revocation would have on the 180 students who

attended the school

- Taking into consideration the difficulty the students would have in

finding a new school immediately before the start of the school year,

and the shortfall in liquid assets that the school had to continue

operating, the court found that the balance of convenience weighed in

favour of grating a stay

- Court ordered a delay of publication in the Canada Gazette until

December 31 to permit an orderly liquidation of assets and permit the

charity to plan operations without status as a registered charity

|

|

58

|

|

Notes

Notes{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}